Berg Insight estimates that connected alcohol detection and monitoring solutions reached an installed base of roughly 560,000 units across North America and Europe in 2025. The figures highlight a niche IoT market where connectivity is being driven less by consumer convenience than by compliance, supervision and safety requirements.

Alcohol testing is not new, but the operational model around it is changing. For decades, many alcohol detection systems have functioned as point-in-time tools: a breath test, a vehicle interlock event, or a supervised check at a fixed location. The connected version of this market adds a different layer: remote visibility, automated reporting and the ability to respond when a test is failed, missed or potentially tampered with.

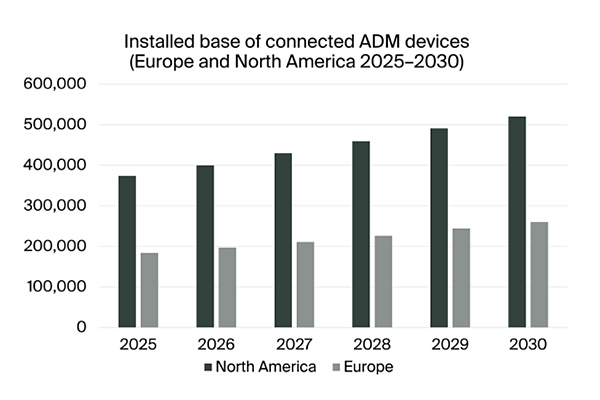

That is the context for new research from Berg Insight, which estimates that the installed base of connected alcohol detection and monitoring solutions reached 374,000 units in North America and 184,000 units in Europe in 2025. By 2030, the research firm expects those figures to rise to 520,000 units in North America and close to 260,000 units in Europe.

The market remains modest compared with mainstream IoT categories such as fleet telematics or smart metering, but it is notable because the connectivity requirement is tied directly to institutional workflows. Berg Insight identifies road safety and transportation, workplace safety, healthcare and rehabilitation, and legal or public safety applications as the main use environments. These are not identical markets, even when they use related sensor technologies.

A compliance-driven IoT category

The largest connected device segment in both regions is ignition interlock devices, which account for around half of the installed base. These systems are mainly used in Driving Under the Influence offender programmes and in workplace fleet safety applications, where a vehicle can be prevented from operating if an alcohol test is not passed. Other connected device categories include smartphone-connected breathalysers, wearable ankle and wrist devices, and wall-mounted or stationary systems used in locations such as probation offices and workplace entrances.

What makes this announcement distinct from many IoT market updates is the nature of demand. This is not primarily a consumer electronics adoption story, nor is it simply about adding connectivity to an existing product line. Berg Insight notes that most alcohol detection devices sold today are still standalone products with limited or no connectivity. The connected segment is therefore a subset of a much older testing market, shaped by regulatory programmes, institutional supervision and workplace policy rather than by mass-market device replacement cycles.

That distinction matters for IoT suppliers. In a consumer breathalyser, connectivity may support convenience or personal tracking. In an offender monitoring, fleet safety or probation environment, connectivity becomes part of the compliance infrastructure. The practical implication is that device makers and platform providers must support event reporting, remote supervision and exception handling, not just sensor readings. A missed test or tampering attempt is operationally different from a delayed data point in a conventional monitoring application.

Regional differences remain important

North America is currently the larger market, with Berg Insight valuing connected ADM solutions there at US$409 million in 2025 and forecasting growth to US$571 million by 2030, equivalent to a compound annual growth rate of 6.9 percent. In Europe, the corresponding market value is estimated at US$187 million in 2025, rising to US$264 million by 2030.

The regional split also reflects differences in programme adoption. Berg Insight notes that only a limited number of European countries currently operate DUI offender programmes, while relatively few US states require real-time connectivity within their ignition interlock programmes. This creates an uneven connectivity opportunity: the installed base can grow not only through new alcohol monitoring use cases, but also through the migration of existing offline or intermittently supervised processes to connected platforms.

For OEMs, the findings point to a market where product design has to reflect deployment context. Wearable devices used for continuous monitoring face different constraints from vehicle interlocks or high-volume stationary testing systems. For connectivity providers, the opportunity is unlikely to be defined by high data volumes; reliability, coverage, device lifecycle management and secure reporting are more relevant. System integrators and public-sector technology partners, meanwhile, may need to connect ADM data to case management, fleet safety or workplace compliance systems.

Berg Insight lists a range of vendors active in the space, including North American companies such as Alcohol Countermeasure Systems, Smart Start, Mindr, SCRAM Systems, BI Incorporated, BACtrack, SoberLink, SobrSafe and Trac Solutions, as well as European providers including Draeger, Innovative Process Solutions, Buddi, Dignita and Senseair. Additional international providers cited include SuperCom, Breatech and Autowatch.

The broader IoT relevance is that connected ADM sits at the intersection of sensing, identity, policy enforcement and remote operations. Its growth will not be determined only by sensor sophistication. It will depend on whether regulators, employers and institutions choose to treat real-time or near-real-time alcohol monitoring as necessary infrastructure rather than an optional add-on to established testing methods.