Berg Insight forecasts that the installed base of water AMI endpoints in Europe and North America will nearly double between 2025 and 2031. The figures point to a shift from mobile meter reading toward fixed-network water metering architectures.

For water utilities, the metering question is increasingly less about whether a meter can communicate and more about how often, through which network, and with what operational consequences. Drive-by and walk-by readings can digitize billing, but they do not provide the same infrastructure for continuous monitoring, leakage detection or near-real-time operational data.

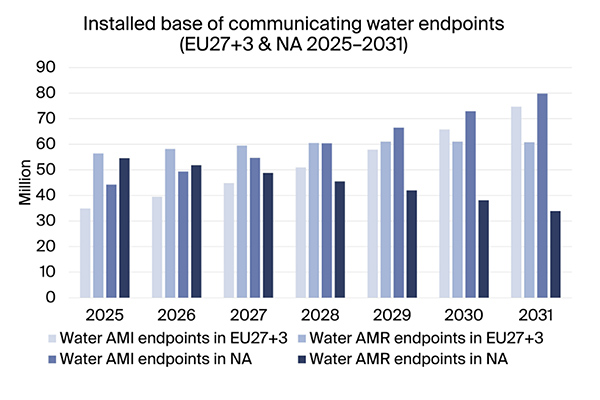

That distinction is central to new market data from Berg Insight, which estimates that Europe and North America had a combined 79.1 million water AMI endpoints installed at the end of 2025. The research firm expects that figure to grow at a compound annual growth rate of 11.8 percent, reaching 154.5 million endpoints in 2031.

The broader installed base of communicating utility water meters, including both AMI and AMR, is forecast to rise from 190.1 million units in 2025 to 249.2 million units in 2031. AMR refers to meters read through mobile operations such as drive-by or walk-by collection, while AMI relies on fixed network communications and supports a more IoT-oriented operating model.

Why the AMI share matters

The most revealing point in the forecast is not simply the headline growth figure. Based on Berg Insight’s numbers, AMI represented about 42 percent of communicating water meters across the two regions in 2025. By 2031, it would account for roughly 62 percent. That implies a structural shift in the installed base: utilities are not just adding connected meters, they are moving a larger share of the market toward fixed-network infrastructure.

This is what makes the announcement distinct from a typical smart metering market update. It separates general meter communications from true AMI connectivity and shows how the center of gravity is moving. For IoT suppliers, that distinction affects module selection, network design, battery-life assumptions, data management and integration with utility systems.

North America remains the largest market for AMR and AMI water metering, according to Berg Insight. Large-scale AMI deployments in the region began gaining momentum around a decade ago, and several projects involving more than 100,000 endpoints have now been completed. Europe is the second-largest market, but its technology landscape is more fragmented.

The connectivity picture is also changing. Proprietary and EN 13757-based RF technologies still lead in both regions, but LoRaWAN and 3GPP-based LPWA technologies such as NB-IoT and LTE-M are identified as the fastest-growing technology categories for new water AMI deployments. In North America, LTE-M is currently the single fastest-growing technology for new deployments. In Europe, LoRaWAN demand is described as more geographically widespread, while 3GPP-based LPWA adoption is especially visible in Spain, where several major utilities have launched large-scale NB-IoT rollouts. Interest in cellular LPWA is also strong in the UK, Italy and the Baltics.

Implications for the IoT ecosystem

For OEMs and meter manufacturers, the forecast reinforces the need to support multiple connectivity paths rather than treating water metering as a single-radio market. A product strategy that fits North American LTE-M demand may not map cleanly onto European tenders where LoRaWAN, NB-IoT, EN 13757-based RF or proprietary systems may all appear depending on the country and utility.

Connectivity providers face a different challenge. Water meters are long-life assets, often installed in locations that are difficult for radio propagation, including pits, basements and underground chambers. The report does not provide performance data, but the growth of LPWA in this segment underlines why deep coverage, predictable service continuity and low-power device operation remain central purchasing criteria for utilities.

System integrators and enterprises working with utilities should also read the numbers as a signal that data infrastructure will become more important than meter reading alone. AMI deployments create recurring flows of operational data that must be integrated with billing platforms, customer service systems, leak analytics and asset management tools. The migration from AMR to AMI therefore shifts complexity from field collection logistics toward network operations and software integration.

Berg Insight identifies Itron, Diehl Metering, Sensus International, Veolia Connected Solutions and Sagemcom among the companies with the largest accumulated installed bases of water AMI endpoints in Europe at the end of 2025. In North America, the top five were Sensus, Badger Meter, Aclara, Neptune Technology Group and Master Meter. Other vendors cited across the two regions include Kamstrup, Honeywell, Minol-ZENNER Group, Mueller Systems, Apator, Maddalena, ADD Grup, Janz, Landis+Gyr and Axioma Metering. SUEZ Digital Solutions is also noted for its role in the development and deployment of Wize technology in Europe.

The forecast points to a water metering market that is becoming more connected, but not more uniform. For IoT companies, the opportunity is substantial; the harder part will be matching the right communications architecture to each region’s utility procurement habits, installed base and operational priorities.