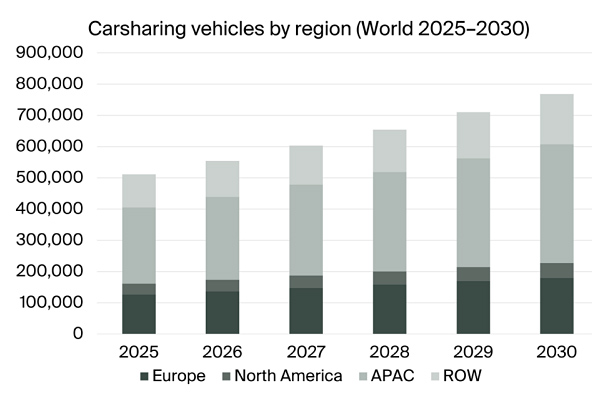

Berg Insight expects the global public carsharing fleet to grow from 511,000 vehicles at the end of 2025 to 768,000 by 2030, with users rising to 141.1 million over the same period. The forecast underlines how telematics, booking systems and fleet operations software have become core infrastructure for shared mobility services.

Shared mobility has often been discussed as a consumer transport trend, but its operational reality is closer to a distributed IoT business: thousands of unattended vehicles, multiple access models, remote authentication, billing, vehicle status monitoring and continuous fleet optimisation. Without connected in-vehicle equipment and software platforms, the modern carsharing model would be difficult to operate at scale.

That is the more relevant signal in Berg Insight’s latest forecast. The analyst firm projects that the number of vehicles used in public carsharing services will increase at a compound annual growth rate of 8.5 percent, from 511,000 at the end of 2025 to 768,000 at the end of 2030. The user base is expected to grow slightly faster, from 91.0 million people in 2025 to 141.1 million in 2030, representing a CAGR of 9.2 percent.

The forecast also highlights the geographical balance of the market. Asia-Pacific accounts for the largest share of carsharing vehicles, followed by Europe. Europe stands out for another reason: free-floating carsharing is the most common operational model there in terms of both membership and fleet size, according to Berg Insight.

Why this forecast is different from a standard mobility growth story

The distinct point in this announcement is not simply that carsharing is expanding. The more important finding is that growth is tied to increasingly specialised connected fleet infrastructure. Berg Insight does not describe carsharing as a market driven only by vehicle supply or consumer demand; it frames it as an ecosystem dependent on in-vehicle telematics, booking management, billing, fleet supervision, dashboards and analytics.

That distinction matters for IoT suppliers. A station-based round-trip service and a free-floating urban fleet place different demands on platforms. Station-based carsharing can rely on fixed return points and more predictable vehicle movement. Free-floating services, by contrast, require operators to manage vehicle availability across a permitted zone, monitor utilisation and support more dynamic operational decisions. The press release does not quantify the technical differences, but the implication is clear: as free-floating models gain importance in some regions, software and telematics requirements become more central to service reliability.

Carsharing operators are not all building this technology themselves. Berg Insight notes that some use in-house hardware and software, while many source products and services from specialised vendors. The market includes suppliers offering end-to-end combinations of telematics equipment and carsharing platforms, as well as companies focused on either hardware or software. Named vendors include Invers, Vulog, Convadis, Targa Telematics, Optimum by Shiftmove, Mobility Tech Green, WeGo Carsharing, Atom Mobility, CT Mobility, Cantamen, MOQO, 2hire, Bosch and Astus.

For OEMs and vehicle technology providers, this points to a practical integration challenge. Carsharing vehicles are not simply connected cars placed into a rental fleet. They must support unattended access, booking workflows, usage-based billing and operational monitoring. The more fragmented the fleet or the more varied the service model, the greater the need for interoperability between embedded hardware, mobility software and back-office systems.

Profitability is reshaping the connected mobility stack

Berg Insight also observes that many operators have shifted their focus in recent years from market share gains toward profitability and higher vehicle utilisation. That change is significant for technology providers because utilisation-driven operations require better visibility into fleet status, demand patterns and asset performance. In this environment, telematics data is not a secondary feature; it becomes part of the business model.

The corporate carsharing segment adds another dimension. Berg Insight estimates that corporate carsharing represented 154,000 vehicles at the end of 2025 and will reach about 250,000 vehicles by 2030. For enterprises, leasing firms and system integrators, this suggests continued demand for shared fleet tools that can reduce manual administration while supporting controlled access and usage tracking across business users.

The operator landscape remains mixed. Specialist providers such as Times Car, Socar, Communauto, Evo Car Share, Miles, Stadtmobil, Cambio, MyWheels, Greenwheels, Enjoy, Mobility Cooperative, Citiz, Traficar, TikTak, Turbi and GoGet operate alongside car rental groups such as Sixt Share, Zipcar, ORIX CarShare and G Car. Carmaker-backed services include Free2move, Kinto Share and Wible. Berg Insight adds that the top 30 carsharing service providers account for around 63 percent of members and manage about 56 percent of the global fleet.

For connectivity providers, the opportunity is therefore not limited to SIMs or data plans. Carsharing fleets require reliable connectivity as part of a broader service architecture that includes vehicle access, fleet visibility and operational control. For IoT platform vendors and integrators, the market’s move toward utilisation and profitability may be more important than headline fleet growth: operators will need tools that help them run fewer idle vehicles, not just connect more of them.